The Virginia State Bar (VSB) is a self-sustaining, non-general fund agency responsible for raising its own revenue, most significantly through its annual membership dues. The VSB receives most of its revenue through annual membership dues payments. The VSB also generates revenue through other sources, such as mandatory continuing legal education (MCLE) course sponsor fees, delinquency fees, section dues allotments, and Virginia Lawyer Referral Service administrative fees and remittances.

Beginning in 1995, VSB annual dues were statutorily capped at $250. On July 1, 2026, HB 276 will become law, and the statutory cap will increase to $350. VSB annual dues for active and associate members, $250 and $125, respectively, have not increased since July 1, 2000.

Part Six, Section IV, Paragraph 11 of the Rules of the Supreme Court of Virginia (Paragraph 11) states the VSB annual dues may not exceed $250 for active members and $125 for associate members.

The VSB plans to update Paragraph 11 in light of the statutory cap increase and is considering the amount that member dues will increase by for the 2027–2028 fiscal year. Members are invited to provide comment on this topic by August 17, 2026. Note: Any change to member dues must be approved by the VSB Council and the Supreme Court of Virginia.

Below is a list of frequently asked questions about this potential increase.

Why must the VSB raise dues?

In short, operating costs have increased significantly, and membership numbers have flattened since the last time dues were raised in 2000. The stagnation in VSB membership numbers has resulted in VSB revenue not keeping pace with its operating expenses, resulting in an unbalanced budget.

Inflationary Increases

The growth in VSB expenditures is primarily due to increases in salaries, technology costs, inflation, and rent.

- Since 2000, salaries have increased 59.5 percent

- Technology demands and cybersecurity costs have risen substantially.

- Since 2000, inflation has risen 87 percent.

- In the past 10 years, rent has increased 28 percent.

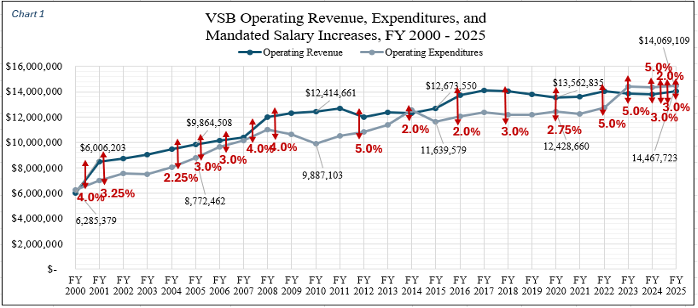

Salaries are the VSB’s most significant operating expense. More than 70 percent of the VSB Fiscal Year (FY) 2026 Budget was allocated to employee salaries and benefits – an increase from 65 percent in FY 2000 and 58 percent in FY 2006. Despite the increase in the proportion of operating expenses attributable to employee salaries and benefits, the VSB has not had a corresponding increase in personnel – the FY 2026 budget included 2 fewer positions than funded in FY 2006.

The data show that General Assembly-authorized salary increases, with the VSB’s primary revenue source capped, are highly correlated with the VSB’s increased expenditures, particularly beginning in FY 2021 where, between FY 2021 and 2025, there were 6 separate raises — adding more than a 20 percent increase in wages1. Chart 1 summarizes the mandated compensation increases, which were well-deserved and earned, alongside each FY’s total operating expenditures and revenue.

Flattening Membership Numbers

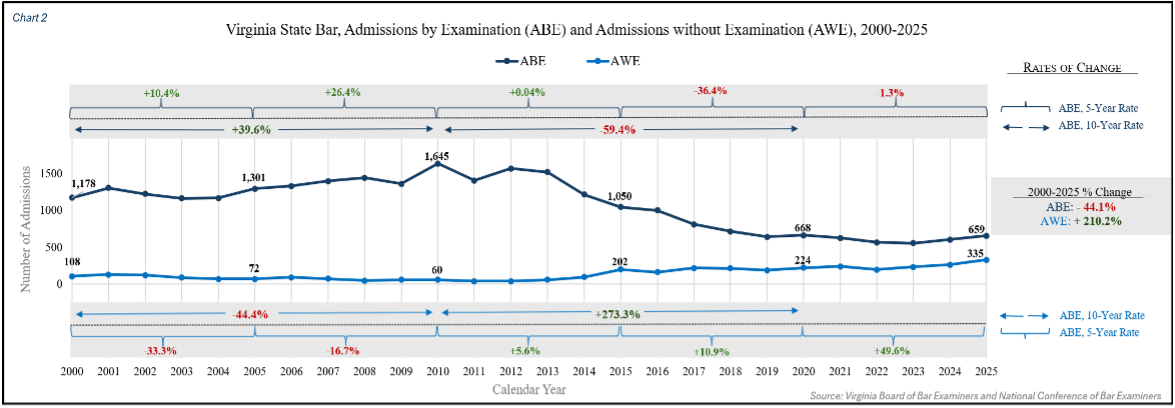

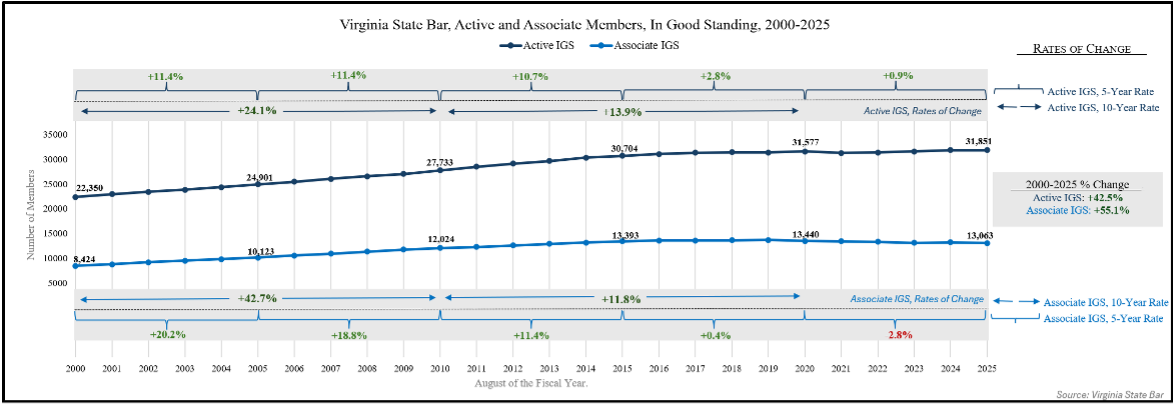

Historically, the number of VSB members generally increased each year, resulting in higher amounts of revenue from annual dues payments—negating the need for a dues increase. However, VSB data show that new VSB admissions are declining (Chart 2) and Active and Associate Membership numbers have flattened (Chart 3).

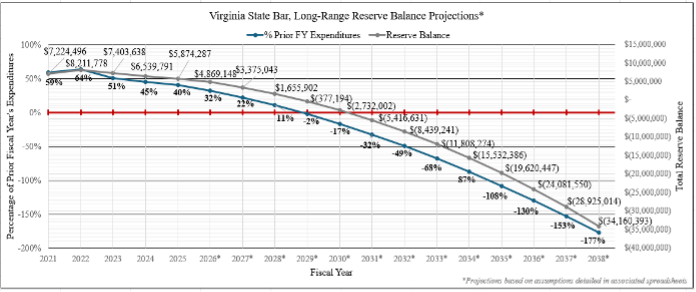

VSB Reserve Fund Depletion

The VSB has used its strategic reserve fund to bridge the gap in the budget. Projections indicate that if member dues are not raised, the VSB will fully deplete its reserve fund by the 2029–2030 fiscal year (Chart 4).